VERIFIED PAYOUT PROOFS · UPDATED DAILY

Every prop firm claims to pay.

Here is the proof.

We track real funded trader payouts from public posts on X and Reddit, verify every screenshot against its source, and log them here. No estimates. No aggregates. Nothing we can't prove.

9:41

TRADERPAYOUT

TRADERPAYOUT

Latest verified payouts

SCREENSHOT-VERIFIED · NEWEST FIRST

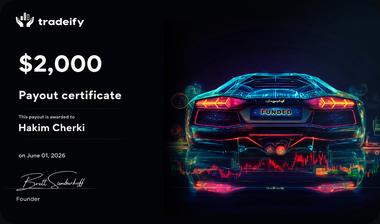

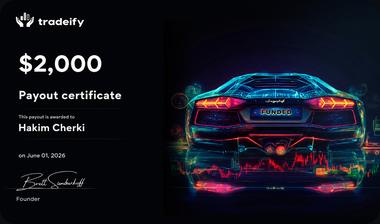

Apr 28@nq_trader_88R$4,820

Apr 27@scalper_jenX$9,250

Apr 25@es_swing_danR$12,180

Apr 21@swing_systemsX$14,420

Apr 23@cl_breakoutR$7,610

Apr 20@gc_levelsR$3,140

Apr 19@mnq_paulaX$6,890

Apr 18@orderflow_maxR$10,540

Apr 16@ict_nadiaX$2,760

Apr 15@vwap_theoR$8,320

Public sources onlyPulled from X and Reddit, never supplied by the firms

Cross-checkedEvery screenshot verified against its original post

Linked to the sourceEach proof carries a link straight back to the post

01

Top prop firm offers.

VERIFIED DISCOUNTS · CHECKED DAILY

1BEST OFFERS

Apex Trader

Funding

Funding

4.8 ★★★★★

TRUST SCORE96/100

0100

PROMO CODEONKAGNVZ

⧉ COPY

90% OFF i

CLAIM DISCOUNT

PropShopTrader

4.5 ★★★★☆

TRUST SCORE85/100

0100

PROMO CODEFUNDEDPROGRAM

⧉ COPY

60% OFF i

CLAIM DISCOUNT

02

Who actually moves the money.

EST. MONTHLY PAYOUT VOLUME SHARE

$50M+ PAID MONTHLY ACROSS TRACKED FIRMS

ESTIMATES · FROM FIRM-REPORTED MONTHLY VOLUMES

03

Inside Trader Payout.

FIVE DESKS · ONE METHODOLOGYProof of payout

Real payouts, traced and verified

UPDATED DAILY

02 · DEALSDiscounts

Best active codes, checked daily

UP TO 90% OFF

03 · LABReviews

Every firm scored on payouts

39 FIRMS

04 · DESKLearn trading

Guides from funded traders

FREE

05 · TOOLSCost Engine

Your real expected cost to funded

NEW

06 · WIREThe Wire

Live verified payout feed

+9 TODAY

04

The Apex files.

LIVE · LAST VERIFIED TODAY 04:25 UTC · 9 NEW IN 24H

PAYOUTS

Verified payouts, two sources.

Browse verified payouts from either the community or Apex's official feed. Community proofs are screenshot-verified payouts collected from public trader posts. Apex payouts come straight from Apex's official payout feed.

Every public proof, archived.

REDDIT · X · DISCORD — SOURCES LINKED · UPDATED DAILY

-

TOTAL PAYOUTS · ALL TIME

-

TRADERS PAID · UNIQUE HANDLES

-

AVG PAYOUT · PER PROOF

-

NEW IN 24H · NEWLY ADDED

Latest verified payouts.

SCREENSHOT-VERIFIED · FROM PUBLIC TRADER POSTS · NEWEST FIRST

| DATE | TRADER | ACCT | SOURCE | AMOUNT | PROOF |

|---|

OUR VERDICT · INDEPENDENT REVIEW

S

Apex Trader Funding review.

Apex accounts for the largest share of the verified payouts in this archive. Read our full breakdown of how it pays, the rules that trip traders up, and whether it holds up.

READ THE FULL REVIEW → AFFILIATE LINK. WE MAY EARN A COMMISSION. VERDICTS WRITTEN INDEPENDENTLY.

⧉ ONKAGNVZ · CLAIM →

AFFILIATE LINK. WE MAY EARN A COMMISSION. VERDICTS WRITTEN INDEPENDENTLY.

⧉ ONKAGNVZ · CLAIM →

READ MORE · APEX DEEP DIVE

8 ARTICLES

COSTS

Apex Trader Funding activation fee: what you pay after passing.

by Kevin Macia

VERDICTIs Apex Trader Funding legit? What the data actually shows.

by Kevin Macia

MECHANICSApex trailing drawdown explained: EOD, Intraday, and the mechanic that ends most funded accounts.

by Kevin Macia

COMPARISONApex vs Topstep: a verified comparison of two futures prop giants.

by Kevin Macia

05

How we verify. Same four steps, every firm.

METHODOLOGY · APPLIED WITHOUT EXCEPTION1

Sourced

Pulled from public posts on X and Reddit, never supplied by a firm.

2

Cross-checked

Amount and date matched against the original post before it logs.

3

Linked

Every proof carries a live link to the source. Follow it and check.

4

Logged

Timestamped with an ID and never edited after publishing.

✓

Apex compensation, reported by the firm.

SELF-REPORTED · VERIFIED JUN 2026$0

TOTAL COMPENSATION TO CUSTOMERS SINCE 2022

$0

AVERAGE MONTHLY COMPENSATION SINCE APRIL 2024

$0

TOTAL COMPENSATION · LAST 90 DAYS

SELF-REPORTED BY APEX TRADER FUNDING · VERIFIED 26 JUL 2026 · PAYOUT PROOFS ARCHIVED ABOVE

06

Which prop firms are actually paying out.

ON-CHAIN · VERIFIABLE ON ARBISCAN?

Questions, answered.

HOW TRADER PAYOUT WORKSAn independent platform that tracks and verifies real payout proofs from funded traders across the major prop firms. Every entry is sourced from a public post, cross-checked against the original screenshot and source URL, and logged only when we can independently confirm it.

Three steps before anything appears on the site: identify the original public post, cross-check the screenshot against the source URL and timestamps, then confirm the firm, amount and account type. If any step fails, the proof is discarded. No exceptions, no estimates.

Every proof is tied to a public post from a real trader handle, with the source URL linked directly on the proof page. If we cannot verify both the source and the screenshot, it does not appear here.

We are independent. Some links, including links to Apex Trader Funding, are affiliate links and are disclosed on every relevant page. Our data collection and verdicts are never influenced by affiliate relationships, and we track firms we have no commercial relationship with.

Daily. Our system monitors public posts continuously and new proofs are added as they pass verification. Counts and statistics reflect the most recent verified data at all times.